|

|

|

The World Economy has Gone Back to Normal

Global GDP growth of only 1% (on top of a 1% inflation rate), no growth in wages, and no pricing power for retail stores many of whom

are racing to the bottom then disappearing. The best investment returns are only 5% but property values in the popular cities are growing

beyond the reach of most families ... it's an economic apocalypse!

Well no it's not. It is the normal behaviour of a stable industrial economy.

The world of high growth and a rapidly improving middle class was an economic blip that

only the Baby Boomers got to experience. The Great Recession of 2007 did not signal the beginning of a "new normal" it

marked the return of the "old normal". Our future for decades to come will follow the pattern set down

by hundreds of years of industrial economy histories.

A Capitalist Economy According to Thomas Piketty

In

"Capital in the Twenty-First Century" (2013) Piketty describes the economic environment

in Britain and France (and to a lesser extent Germany and the USA) from 1700 to today. He shows that

the long term real growth rate (g) is 1% (after inflation) and the long term investment return or rent (r)

is 5% (after inflation). He also makes a good case that this not just our near future but the behaviour of the global

economy for the next hundred years.

When I quote a source I always advise the reader check my facts. This is difficult with

"Capital in the Twenty-First Century" because it is not an easy book to read. It's kind of

"War and Peace" with math and data tables. At 696 pages it is only half the size of "War and Peace"

but as an economics textbook it lacks the character development of a work of fiction. It is on the list

of popular books that are purchased but never read. I found it

to be a real page turner ... but that's just me.

The statement in Capital that gets the most attention is that r > g means the rich will always get

richer. More important r > g is an inherent property of capitalism. In a free market without

any government interference the "invisible hand" of Adam Smith's marketplace will enforce this

inequality.

The math is easy. If you have an asset that pays a 5% compound interest it will double in value

in 14 years. A child that inherits $1 million will see that investment double 5 times by

their 70th birthday when it will be worth $32 million.

Meanwhile the country is only growing at 1%

so the GDP will double in 69 years. The wealth of an average person only grows at the rate of the GDP.

So the average child with a $100,000 share of the family assets at birth will be worth $200,000 at age 70.

The rich child who starts with 10 times as much will be worth be 160 times the average child by age 70.

...but Growth Will Return Won't It?

Piketty also shows the two world wars resulted an massive destruction of global assets. He shows

that an economy "remembers" the asset value that a 1% growth would have achieved if there had been no

disturbance (like war). After the chaos it will race to get back on that 1% long term trend line.

At the end of WWII the economies of Britain, France, Germany, and Japan were destroyed along with their cities. They raced to

rebuild their lost assets and the (non-destroyed) USA economy supplied that growth and profited greatly. That plus the added population from the Baby Boom meant world GDP growth

was over 5% for 30 years and 3% for another 20. Piketty's r > g held but not so dramatically for most

of this time and new wealth was evenly distributed through the population. The result was an affluent middle class.

The Great Recession was not caused by the 2007 financial collapse it simply marked the

return to a g of 1%. It could be argued that the financial bubble was caused by a belief in a

return to a 5% growth in GDP. Large sums were borrowed under the assumption that the debtors could

grow themselves out of trouble. After years of low growth the loans came due and defaulted.

Governments too were convinced that 5% GDP growth was normal and pumped huge amounts of cash into their economies.

When nothing happened they were puzzled but continue to promise that "5% growth is coming soon".

Since 1950 printing money caused a quick jump in economic activity and the demand for scarce resources that

led to punishing inflation. Central banks could manage the balance between growth and inflation

and fine tune the process by fixing the interest rate.

That changed in the 2000s. Monetary policy the primary tool of the central banks no longer works. The $trillions now flooding

the world economies should have ignited a massive jump in GDP and recent history predicted we should

now be suffering the 15% inflation we saw in 1980.

Fiscal stimulus shows the same problem. A government sells bonds to those who have "spare" cash.

Governments use the borrowed money to build infrastructure (added wages and materials) and grow the economy.

The theory is that GDP growth increases tax receipts so they can pay back the loans.

What worked well when recovering from WWII destruction now fails. The GDP remains stubbornly at 1% (g) yet governments need to

pay the going rate 5% (r) to the bond holders. Without large GDP growth governments fall deeper into debt

with each bond issue. The only way to get a lower cost of borrowing is to sell government bonds to their own

central bank (quantitative easing).

A central bank doesn't have to borrow money it just prints it ... or in our digital age increase

a counter in some central bank account. Once again the economy sees freshly printed money as a

"reverse mortgage" that gets consumed at a 5% (r) until the entire amount is transfered to wealthy individuals.

Rents from bonds issued by governments or central banks are used by the

bond holder to buy real assets. Since the largest real asset is real estate the

result is a rapid increase in property values. The GDP grows at 1% and property values grow at 5%.

So we are now in the new/old normal state. Global real GDP growth struggling to reach 1% (the often quoted 2%

GDP growth must be discounted by 1% inflation).

Wages should at least grow the 1% inflation rate but productivity growth (more goods for less labor)

is small but just enough to keep wage growth at 0%.

The safest investment returns are only 5% but the middle class has

no money to invest. Meanwhile the 5% compound growth in property values (an r affected investment) is leading

to prices far beyond what the middle class can afford.

A Note on Productivity

The promise has been that an increase in productivity benefits everyone. "Labor productivity"

is defined as "output volume" / "labor inputs". If productivity increases more widgets can be created for fewer

labor hours. The theory is the workers made surplus can go on to better jobs and those remaining can be given

an increase in pay.

You start off with ten men with shovels and a foreman to dig a ditch. You replace that with a man

in a backhoe, a traffic control person and a part time foreman. In the near future you replace that with

a self-driving backhoe and scheduling software. In theory all the surplused people become computer programmers and make $200,000 per year.

In a rapidly growing economy there is always a shortage of labour. Any surplused employee has their pick

of many new jobs. The competition between employers mean they get higher wages.

When the GDP is only growing at 1%

there is nothing for the surplused workers to do. The supply of labor exceeds demand and with a large number

of applicants for each job employers can take the lowest bidder.

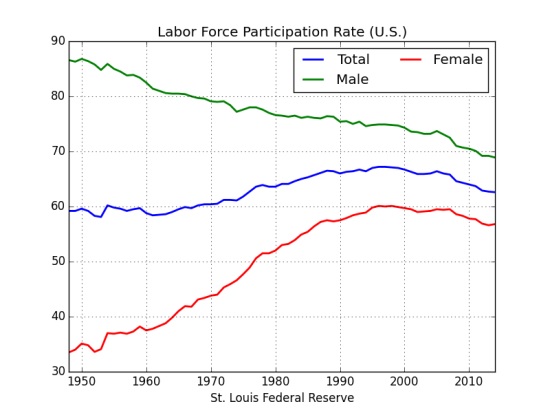

The result is that "Labor Force Participation Rate" (percent of available workers actually working) has been declining

and men have been hit the hardest because they used to have all the jobs.

With an excess supply of labor the impact on wages is economics 101. The price (wage) will drop until those desperate to work will

take the job. The impact is that growing productivity causes stagnant wages:

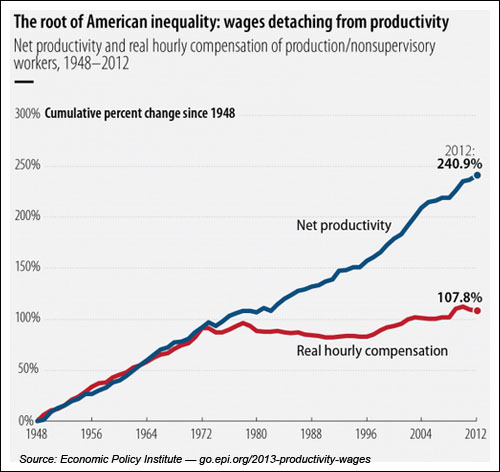

The problem with the current economy is not "poor productivity". Productivity appears to be fixed at 3.75% per year (perhaps a property of

stable market capitalism like r=5% and g=1%). When GDP growth is less that than 3.75% wages are flat. In the "new normal" no wage growth

means the improved productivity that is hollowing out the middle class will continue its cruel progress.

Fitzwilliam Darcy Investing

I mention Darcy because Piketty uses him as an example of a wealthy man in a "normal" economy.

In Jane Austen's novel "Pride and Prejudice" (1813) Darcy is the love interest of Elizabeth Bennet. He

is known to be a very wealthy man with an income of 10,000 per year. Nothing is said of his wealth.

In fact everyone is measured by their income not their balance sheet.

In Jane Austen's world your net worth is unimportant. Only investment income matters. The average wage is

so low that is is not socially important (the village doctor does not make much more than the blacksmith).

An asset has no other value than the rent it generates. Non-performing assets have no social value.

In the new normal we will gradually drift into this metric. The flood of cash will increase

the cost of all assets. A person in a $2 million home is rich but unimportant. If they have

no income they are less than important because they won't keep their expensive home for long.

A person with $1 million in investment income is someone you should pay attention to. In 14 years

they will have an income of $2 million a year.

So what does Darcy do all day? In Austen's book he is a busy man. Busy doing what?

Darcy takes most of his 5% rent income and buys new assets to increase his income.

He is a "buy and hold" investor because he is only interested in the rent. He finds a property that is

not doing well and puts in the hands of employees he trusts. They run the asset so it produces the best rent possible. That

makes him "value investor". He lives in a mansion (Pemberly) but even it generates rent from the surrounding

lands.

In summary: Darcy is a "buy-and-hold, rent-only, value-investor".

Darcy is a prudent man who is aware of the value of everything which means he measures assets based

on the rent they can generate. This is the source of both his pride and his prejudice. In Austen's

story he is persuaded to see Miss Bennet as a different kind of asset ... but that is a story

for another webpage.

Eugène de Rastignac a Cautionary Tale from Balzac

Piketty uses a story from Balzac to show how difficult it is to move into the ranks of the rich without

income from an inheritance.

In "Père Goriot" (1835) Balzac introduces an ambitious lawyer Eugène de Rastignac who wants to become

rich. He is told by a criminal named Vautrin that without an inheritance there is no way he can get

rich. Vautrin explains that after decades of a brilliant career in law and some political dirty

tricks Rastignac might be named to one of the twenty prosecutor-general posts in France. Even then he can only

expect to retire into small cottage on a small pension.

Vautrin tells Rastignac if he wants to be rich he'll have to marry into a rich family. Without

rent from investments to cover his living costs and give him extra to grow that investment he will always

be poor. The story goes on to a criminal scheme to marry an ugly heiress and murder her brother

making her the sole heir to the estate (effective perhaps but not the investment advice of this webpage).

The cautionary part is that Balzac's math is true in today's economy. If you want to have enough to cover

your costs and have some left over to invest you will probably need an investment income of $50,000 per year.

At the new normal of 5% you will need to start with $1 million. Sadly if you are starting with $0 in assets you should

prepare to retire into a small cottage on a small pension.

Piketty calculus makes it clear that the Baby Boomers are the last generation that could

start with $0 assets and make into the Darcy's "investor class".

Sooty's advice: If you are

lucky enough to inherit a $1 million from your Boomer parents don't piss it away on SUVs, fine wine and

vacations ... get it generating rent before you spend a penny of it.

2018 is not 1816 - Balzac Revisited

In the 1800s there was no 'technical' class. Balzac chose Rastignac because in French society lawyers were

relatively well paid and well respected. If a lawyer could not make the leap to "rich" there

was little hope for anyone without an inheritance.

If you started your career in 1970 and you knew

something about investing (missing from the high school curriculum) there was a pretty good chance you could get to

the $1 million mark before you retired. The fact that 95% of the Boomers will not retire with $1 million

is a failure of the education system not the times.

If you are making less than $80,000 a year expect the small cottage as an outcome. Sadly the median

income in Canada is only $31,000 ($76,000 for families) so most of you reading this page don't need an

investment strategy ... you need to marry into a rich family.

Getting to Rich in a Piketty Economy

You will probably need to have a job that requires a university degree in an

applied science (engineer) or some kind of post graduate degree (lawyer, MBA) to get to an income

well beyond modest living expenses ($50,000). If you managed to

get that level of education without a massive student loan (paid for by Boomer parents?) you

might have a chance of joining the rich starting with $0 asset and only a wage as income.

If you write a popular song, sell a lot of something (Ron Popeil), or become a sports superstar (NFL, NHL, NBA, YouTube)

you might have the income to become rich without an inheritance. The chances of that are less than winning a lottery.

Your best bet is a high paying job and a long range plan.

If you are clearing $70,000/year after taxes (engineer) and live on $50,000/year you can put $20,000 into

5% investments and you will have $1 million in 25 years.

If you are clearing $100,000/year (pharmacist)

and put $50,000 into 5% investments you will have $1 million in 14 years.

Today Rastignac could join the ranks of the rich. As an ambitious lawyer with a median starting salary of $66,000 he could work hard,

grow his salary (and investment portfolio), and still marry the cute (but penniless) receptionist with Elizabeth Bennet assets.

Some Parting Advice

Make sure you get all of the r=5%

...don't buy mutual funds and pay 3% in administrative fees (TER).

Make sure the income is tax sheltered

...30% income taxes (the last dollar earned) will cripple your path to rich.

If you want a 5% set-and-forget investment with no administration fees take a look at

Sooty's Investing in Canadian Banks.

If you want a more aggressive investment strategy read the cautions in

Investing 101: What Your Investment Advisor Doesn't Tell You.

|